This way, companies can set a benchmark for themselves and monitor their costs against a budget. Similarly, variance analysis can also help in more advanced analysis rather than limiting the process to a specific area. Usually, standards may differ depending on each type of standard cost. Once companies establish a standard cost for products or services, they can use it to control and monitor their operations.

- Variances are favorable if the standard amount is more than the actual amount.

- However, these present a single-dimensional view of variances for companies.

- Lastly, they can investigate these differences to identify the reasons behind them and control them in the future.

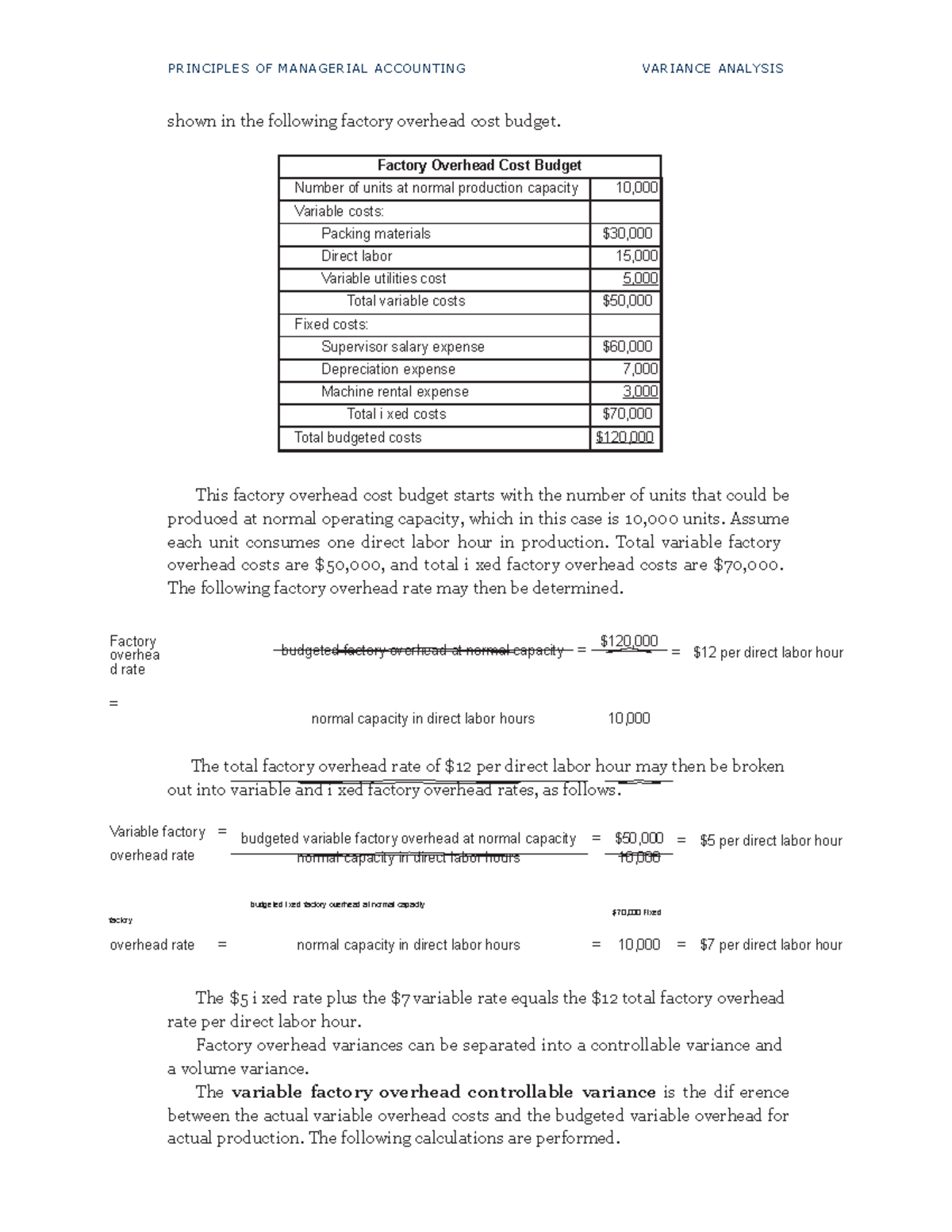

Determination of Variable Overhead Rate Variance

Variance in Accounting is the difference or variation between actual and standard costs. It could also be the difference between the budgeted and actual costs. Depending on whether the actual result was better or worse than projected, variations can either be positive or negative.

Do companies investigate all variances?

This could occur because of inefficiencies of the workers, defects and errors that caused additional time reworking items, or the use of new workers who were less efficient. Actual cost of production may be different than standard cost if any of the five goals listed above is either not met or exceeded. If any one of the quantities or dollar amounts is higher than its standard, the result for that amount is said to be unfavorable since more was consumed spent than was planned.

Variance Analysis in Management Accounting

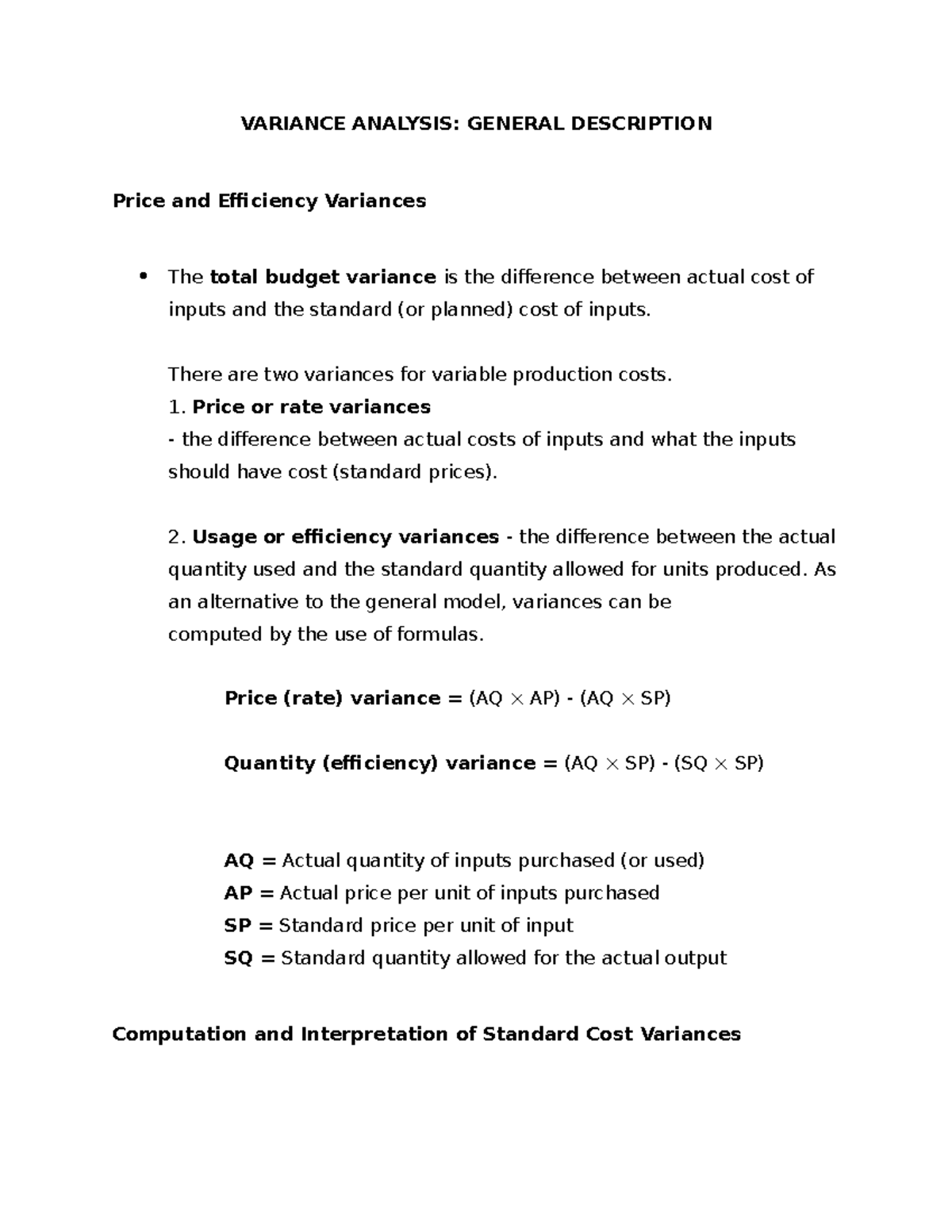

The total direct labor variance is the total standard labor costs allowed of $675,000 less the actual amount paid for direct labor of $832,500, which is $(157,500) unfavorable. At the highest level, standard costs variance analysis compares the standard costs and quantities projected with the amounts actually incurred. Standard costs and quantities are established for each direct material. These standards are compared to the actual quantities used and the actual price paid for each category of direct material. Any variances between standard and actual costs are caused by a difference in quantity or a difference in price. Therefore, the total variance for direct materials is separated into the direct materials quantity variance and the direct materials price variance.

This means that the amount debited to work in process is driven by the overhead application approach. A variance in accounting is the difference between a forecasted amount and the actual amount. Variances are common in budgeting, but you can have a variance in anything that you forecast. Basically, whenever you predict something, you’re bound to have either a favorable or unfavorable variance. The direct labor variances for NoTuggins are presented in Exhibit 8-7 below.

How confident are you in your long term financial plan?

Any discrepancy between the standard and actual costs is known as a variance. Standard variances are considered a red flag for management to investigate and determine their cause. For example, if the actual cost is lower than the standard cost for raw materials, assuming the same volume of materials, it would lead to a favorable price variance (i.e., cost savings). However, if the standard quantity was 10,000 pieces of material and 15,000 pieces were required in production, this would be an unfavorable quantity variance because more materials were used than anticipated. On the other hand, usage or efficiency variances come due to the actual and anticipated production units being different.

It is like a trusted map, leading them to success in today’s dynamic business world. Budgets are the result of planning efforts to estimate a company’s performance tax deductions guide 20 popular breaks in 2021 for a period of time in the future. They are tools that guide managers and employees for keeping operations on track to achieve stated goals.

An unfavorable outcome in this example would be if 8,900 pounds were used in production when only 8,600 were budgeted. A quantity or unit cost is favorable when it is lower than what was anticipated. A favorable result would be if $9 per labor hour were spent since it is lower than the anticipated amount of $10 per hour. If the actual quantity of direct materials is higher than the standard once, the variance is unfavorable. An unfavorable labor quantity variance occurred because the actual hours worked to make the \(10,000\) units were greater than the expected hours to make that many units.

Standard cost projections are established for the variable and fixed components of manufacturing overhead. Manufacturing overhead includes all costs incurred to manufacture a product that are not direct material or direct labor. The total amounts for direct materials actually purchased and used are reported on the following line. The actual quantity purchased and used to produce 150,000 units was 600,000 feet of flat nylon cord costing $330,000.

These welders may have used more welding rods and had sloppier welds requiring more grinding. While the overall variance calculations provide signals about these issues, a manager would actually need to drill down into individual cost components to truly find areas for improvement. Note that there are several ways to perform the intrinsic variance calculations. One can compute the values for the red, blue, and green balls and note the differences.

قم بكتابة اول تعليق